Infinite Banking

Infinite Banking

This is the Agent Training Page for Trifinity Merchant Services

About Infinite Banking For Trifinity Agents

This is for Agent training and is Not for Sales

Infinite Banking

Have you been keeping up with the News?

Today is May 2023 and this week made the 10th straight meeting The Federal Reserve raised interest rates to reduce liquidity to the financial markets and tamp down high inflation.

High Interest Rates are bad for Banks but Great for Insurance Companies. Banks fail and Insurance Companies grow.

Over the last few years creating your own Infinite Bank has become a financial fad!

“Once I set one up for one person they told someone, who told someone and it has become huge for my insurance agency”

Are You Offering Your Customers Infinite Banking?

Chances Are They Have Heard About Infinite Banking and Want To Know More About It

What is Infinite Banking?

Infinite Banking is a concept, that in the past, has been utilized a lot by the Wealthy that can be used by the middle class as well.

It is designed around using Life policies that experience a guaranteed rate of growth, plus dividends as well as favorable tax benefits.

Once an Infinite Banking Account has been established and funded, the owner can borrow from their account by entering into a private contract with their insurance company. The borrower avoids many of the hoops, fees, credit checks, of traditional loans.

Who Created the Infinite Banking Concept?

Who Created the Infinite Banking Concept?

The term Infinite Banking was originally created in the 1980s by Nelson Nash, with his book “The Infinite Banking Concept – Becoming Your Own Banker”.

However, it has been documented that the wealthy, such as J.C. Penney, Ray Kroc, and Walt Disney used similar Whole Life products to either start, grow, or save their business long before Nelson Nash’s work was published.

Through Trifinitys You Can Offer Infinite Banking To Customers Without A Lot of Training!

Financial Planners have used this financial strategy for people looking to build wealth for years!

Does the Infinite Banking Concept Work?

Infinite Banking can indeed work quite well assuming the following:

You Obtain The Right Life policy designed with necessary riders;

You Fund your Policy to the Maximum, Early and as Often as is Allowable;

You make regular loan payments as often as you can;

You seek to utilize your best loan option available;

You expand the strategy as cash flow allows;

Most Importantly

You Deal With An Infinite Banking Specialist Who Knows What They Are Doing.

Some of The Benefits of Infinite banking!

Easier to get a loan – Compared to traditional loans an Infinite Banking Loan are quick, and easy to get, since you are borrowing from yourself! You can borrow your own money without any explanations or credit checks.

Tax advantages – Infinite banking also has tax benefits. Policy loans are traditionally tax-free. On top of this, whole life insurance policies enjoy Tax Advantaged Interest Growth. Additionally, in the event of death, the balance goes to your beneficiary tax-free and often exempt from estate taxes!

Asset Protection – The policyholder enters into a private contract between them self and their insurance company. The privacy of that agreement often comes with benefits for the policyholder such as protection from creditors, judgments, search and seizures. Plus, this won’t impact your credit score.

Learning and Understanding Infinite Banking can be Quite Intimidating to Agents

The Infinite Banking Concept can be confusing at first to the customer and to the Agent as well.

Because of this, Agents will be working with an Infinite Banking Specialist, Karl Schilling.

Acknowledged Infinite Banking Specialist, Karl Schilling, who has written several books on Infinite Banking including:

“Middle Class Millionaire Plan”

This Enables Insurance Agents the Opportunity to offer Infinite Banking

To their Clients with an Infinite Banking Specialist to Guide Them!

Trifinity’s New Card Concept Increased The Sales Potential for our Agents and Huge Savings For Business Owners!

Meet Karl Schilling and New Card Concept

The New Card Concept

While it usually may not properly fund the Up-Front Money necessary to begin an Infinite Banking Plan the New Card Concept will enable Business Owners to make continual funding into their Infinite Banking Plan without that money coming out of the Business Owner’s pocket!

Virtually all Business Owners take Card Payments.

If the Business Owner will give the Insurance Agent 5 Qualified Leads they earn what is called Introduction Commissions!

Qualified Leads are other Business Owners they know and who they will either call or give you a handwritten note that introduces you as someone the other Business Owner will want to talk to about something that they are doing and think the other Business Owner will be interested in doing!

By giving you the 5 Introductions and agreeing to charge 4% instead of 3.5% they can earn the difference in Card Fees as “Introduction Commissions” paid directly into their Infinite Banking account for their retirement!

The Agent will make GREAT commissions on the Life Sale to set up the Infinite Banking Account AND the Agent also earns Residual Commissions every time someone make a Card Purchase!

With Trifinity’s Infinite Banking Specialist, Karl Schilling, guiding you, this will be a Win for the Business Owner and a Win for you the Agent!

Need to make a picture of drawing of card processing with arrow to business owner with arrow to drawing of a Bank!

Karl Schilling

Recognized Infinite Banking Specialist and Founder of the Advocacy Network

Karl Schilling is a recognized Infinite Banking Specialist and Founder of the Advocacy network has over 44 years’ experience in the Financial Services, Resort Real Estate, Business and The Sales Coaching industries.

Karl was one of the initial certified trainers for the classic Earl Nightingale Lead the Field program.

In one year Karl Schilling raised over $23M in capital for small micro-cap issuers. Presently he consults both public entities on rasing capital raise concepts as well as those seeking to go public.

- Founder of the Advocacy Network

- Author of 3 acclaimed books

- Certified Financial Education Instructor

As Agents learn by reading Karl Schilling’s newest book Middle Class Millionaire Plan, Karl Schilling is a Master of Infinite Banking.

Agents Don’t Have To “Reinvent The Wheel”

They Can Take Advantage of The Pros at Trifinity Merchant Services

As Dad Always Said: “Before You Try To Sell Something, You Need To Know A Little Bit, About What You Are Selling”.

Following is Information About Infinite Banking You Might Want To Know

Infinite Banking is a wealth strategy that utilizes dividend-paying whole life insurance as an alternative to saving and borrowing with a traditional bank.

While there are several benefits to using a whole life insurance policy as your private bank, perhaps the two biggest draws are its tax advantages and guaranteed growth compared to a bank savings account, CD, or share certificate. Namely, you can often expect a greater rate of return—plus potential dividends—and you can access this growth without owing taxes.

Does this sound too good to be true?

Well it very well could be.

Most whole life insurance policies aren’t structured to support Infinite Banking, meaning they grow Cash Value incredibly slowly.

The slower your policy accumulates wealth, the less advantageous it is and the longer it takes before you can use your policy to fund purchases, investments, or your retirement.

However, with a properly structured policy, reducing reliance on traditional banks and protecting your wealth from market volatility can happen sooner than you think.

So what’s the secret to a successful infinite banking system?

An Actual Infinite Banking Account Set Up Correctly!

You need to know the difference between an average Whole Life Insurance Policy and properly structured Dividend Paying Whole Life Policy in a correctly set up Infinite Banking Account.

We’ve all heard the old adage: “You have to spend money to make money.”

The Infinite Banking Account helps you spend less money to make money by recouping lost interest. The value of your Infinite Banking Account continues to earn a guaranteed rate of return regardless of outstanding loans!

In other words, when you borrow a dollar through your Infinite Banking Account you continue to earn interest on that dollar at the same time.

Often, the value of your Infinite Banking Account accumulates a greater value than the cost of loan interest, netting positive growth even while paying off a loan.

An Example of an Infinite Banking Plan At Work:

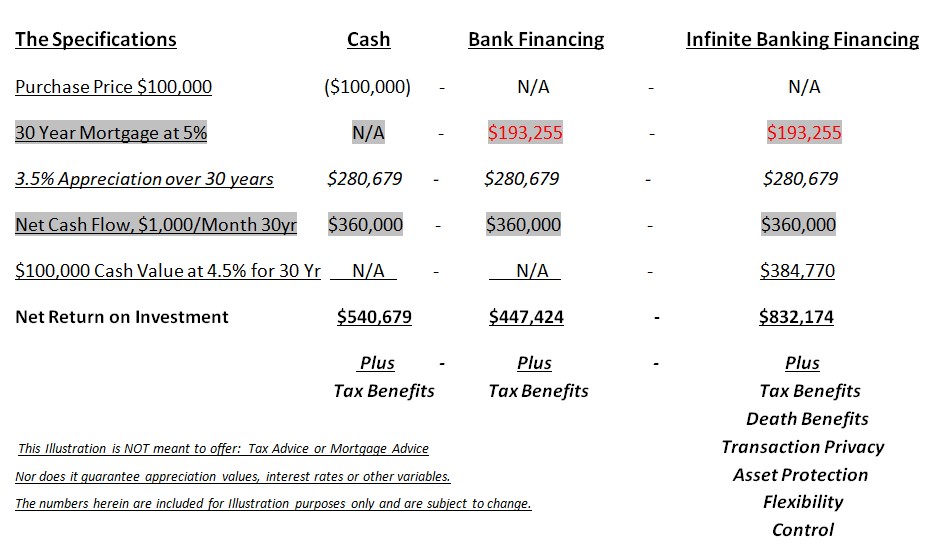

To illustrate the Infinite Banking Concept at work, the example below demonstrates how using Infinite Banking helps grow wealth compared to a traditional bank loan or cash payment for a rental property:

Buying Rental Property: Cash vs Bank Loans vs Infinite Banking Loan

Concerning all the illustration in the training program they are not is not meant to offer tax advise or mortgage advice nor does it guarantee appreciation values, interest rates or other variables. The numbers herein are included for illustration purposes only and are subject to change.

While all three forms of investments have Tax Benefits, the Infinite Banking also has Tax Benefits plus Death Benefits, Transaction Privacy, Asset Protection, Flexibility and Control!

Also with a Bank Loan for a Rental Property the borrower will probably have to put 10% 20% or even more down, with an Infinite Banking account the borrower could loan themself as much as they have in the Cash Value!

Purchasing a rental property with cash means the buyer doesn’t have to pay any mortgage interest, and will earn nearly $100,000 more than a buyer using traditional bank financing, as a result. However, the buyer using the Infinite Banking Concept who takes out a loan from their personal ‘bank’ with a value of $100,000 earns a guaranteed rate of return (4.5% in this example) that nets $384,700 additional dollars over the 30-year mortgage.

The buyer is borrowing their own money ($100,000) and earning interest on it at the same time, making it a more lucrative option than buying the property in cash.

In fact, the buyer using the Infinite Banking Concept earns hundred of thousands more than the cash buyer.

Another benefit Infinite Banking has over a cash purchase would in the event of the Account Holder dying the built in Death Benefit would pay off the Loan so the Beneficiaries would receive the asset Debt Free.

Advantages of Infinite Banking?

Infinite Banking is not a rapid money making scheme. Infinite Banking in its truest form is control over your money and the elimination of unnecessary money leaks from your own personal economy, so that you can utilize your money to grow and increase your assets.

Infinite Banking requires you to take responsibility for your own financial future, and for the goal-oriented individual it can be one of the best financial tools you’ll ever find. Here are the advantages of Infinite Banking:

Liquidity

Arguably the single most beneficial aspect of Infinite Banking is that it improves your cash flow. You don’t need to go through the hoops of a traditional bank to get a loan; simply request a policy loan from your insurer and funds will be made available to you. Whole life insurance is an extremely liquid asset compared to other assets like real estate, stocks, bonds, or qualified plans like your 401(k) or IRA.

Because whole life insurance is liquid, it can make up a valuable part of your financial foundation, acting as your emergency savings. Whether you run into unforeseen medical bills, job loss or costly home repairs, policy loans offer peace of mind. You can even use your insurance policy to pay yourself an income if you decide to go on sabbatical, return to school or take time off work to care for loved ones.

At Paradigm Life, we advocate funding a whole life insurance policy as a savings vehicle before considering other investment strategies like real estate or the stock market as part of our Perpetual Wealth Strategy™, and refer to this type of portfolio structure as The Hierarchy of Wealth™.

Control

Dividend-paying whole life insurance is very low risk and offers you, the policyholder, a great deal of control. The control that Infinite Banking offers can best be grouped into two categories: tax advantages and asset protections.

Tax Advantages

One of the reasons whole life insurance is ideal for Infinite Banking is how it’s taxed. In addition to tax-free policy loans and tax-free growth of interest and dividends inside your whole life insurance policy, the death benefit of a whole life policy is tax-free to your beneficiary and often is exempt from estate taxes as well.

Asset Protections

When you use whole life insurance for Infinite Banking, you enter into a private contract between you and your insurance company. This privacy offers certain asset protections not found in other financial vehicles. Although these protections may vary from state to state, they can include protection from asset searches and seizures, protection from judgements and protection from creditors. Plus, any policy loans you utilize won’t affect your credit score.

Protection Against Volatility

Whole life insurance policies are non-correlated assets. This is why they work so well as the financial foundation of Infinite Banking. Regardless of what happens in the market (stock, real estate, or otherwise), your insurance policy retains its worth.

Too many individuals are missing this essential volatility buffer that helps protect and grow wealth, instead splitting their money into two buckets: bank accounts and investments. The problem with this approach is that, while money in a bank account is safe, it offers a very low rate of return. Market-based investments grow wealth much faster but are exposed to market fluctuations, making them inherently risky. What if there were a third bucket that offered safety but also moderate, guaranteed returns? Whole life insurance is that third bucket.

Regardless of how diversified you think your portfolio may be, at the end of the day, a market-based investment is a market-based investment. In the event of a market downturn, you lose money. Maybe a lot. Maybe a little. Maybe your value doesn’t decrease but your returns do. With Infinite Banking using properly structured whole life insurance, your returns are guaranteed and your cash value won’t decrease.

Certainty

Not only is the rate of return on your whole life insurance policy guaranteed, your death benefit and premiums are also guaranteed. These certainties are another reason why properly structured whole life insurance is the ideal tool for Infinite Banking.

Consider other assets, like those associated with your 401(k) or IRA. In the event you pass away with money left in either of these qualified plans, the remaining funds will be passed onto your beneficiary—but first it will be taxed. You can guarantee your beneficiary will receive something but you can’t be certain how much, due to future tax rates.

While there are other types of permanent life insurance, whole life insurance is guaranteed to have the same premium for the duration of the policy. You can be certain your premium won’t increase as you get older. This is invaluable when it comes to setting and achieving your financial goals.

Cash Flow

Many individuals rely on Infinite Banking for a tax-free retirement. Because insurance policies are paid for with after-tax dollars, you don’t have to worry about your future tax rate like you would with a 401(k). So long as you utilize the policy loan feature of your whole life policy, you don’t have to pay taxes on the growth of your cash value. Simply fund your retirement with policy loans and your insurance company deducts the outstanding loan from the death benefit after you pass away.

When your retirement funds are linked to market-based investments, running out of money in retirement is a very real and valid concern for millions of Americans. Infinite Banking using properly structured whole life insurance can ensure you won’t run out of money in retirement, because your cash flow won’t be at risk if the market experiences a downturn. For this reason, some individuals opt to stop funding qualified plans like 401(k)s or IRAs all together and rely solely on the Infinite Banking strategy for retirement.

Legacy

Infinite Banking with whole life insurance is a proven method for building generational wealth, in part because the death benefit is tax-free and generally not subject to estate taxes.

In the case of large estates where federal or state estate taxes may kick in, it’s possible to utilize Infinite Banking inside of an Irrevocable Life Insurance Trust (ILIT). By naming the trust as the policyholder of your whole life insurance policies, even the largest of estates can be eligible for tax advantages that provide significantly more wealth to future generations.

What Are the Disadvantages of Infinite Banking?

Infinite Banking isn’t a one-size-fits-all strategy. It’s highly customizable and its effectiveness depends largely on your financial goals. Here are three aspects of Infinite Banking to consider when deciding if it’s right for you:

Qualification

Because Infinite Banking uses whole life insurance as its “bank”, it isn’t an option for everyone. You must be able to qualify for a life insurance policy. Qualification is based on your health and age.

Up to about 50 years old Dividend Paying Whole Life is usually the the best option for someone in good health however over 50 similar types of products are available through Annuities.

We work with the nation’s top mutual insurance companies and can help match individuals interested in the Infinite Banking strategy with insurance companies most likely to approve their application. While it’s recommended to apply for a policy when you’re young and healthy, it’s possible to get insured even in retirement—you’re never “too old” to pursue the Infinite Banking strategy.

Cost

Compared to term life insurance, the premiums for whole life insurance are significantly higher. Keep in mind that you’re not just paying for insurance; you’re effectively committing to contribute a set amount into “savings” inside your insurance policy to be used by you whenever you choose while still earning a guaranteed interest rate and potential dividends.

That said, Infinite Banking isn’t ideal for someone living paycheck to paycheck. It requires an individual who is comfortable with saving a significant amount of income and who is focused on long-term financial goals.

Remember, when you utilize the Infinite Banking strategy using whole life insurance, your insurance policy’s primary purpose isn’t the death benefit, it’s the living benefits. Your main goal isn’t protecting your loved ones financially if something were to happen to you—that’s an added bonus. What you’re really protecting is your income. You’re shielding your wealth against bank interest rates and financing, market volatility, creditors, and taxes.

Mindset

Infinite Banking is a proven concept for growing and protecting wealth, but it’s not mainstream. You need to be comfortable with taking your financial future into your own hands and have a clear outline of your financial goals. You also have to be a good banker!

If you don’t pay back your policy loans (with the exception of using policy loans to fund retirement), you won’t see your wealth grow over the course of your lifetime and you be able to create generational wealth.

Does Infinite Banking Really Work?

Yes. The strategy behind Infinite Banking—using dividend-paying whole life insurance as your own personal bank for growing and protecting wealth—is proven to work, and has been used by families for hundreds of years. As with any financial tool, the benefits are largely dependent upon how the tool is used and requires clearly outlined goals to measure success.

For the fastest growth and optimal benefits, it’s recommended to pair dividend-paying whole life insurance with supplemental insurance called a Paid-Up Additions rider (PUAR).

A PUAR allows you to “overfund” your insurance policy right up to line of it becoming a Modified Endowment Contract (MEC). When you use a PUAR, you rapidly increase your cash value (and your death benefit), thereby increasing the power of your “bank”. Further, the more cash value you have, the greater your interest and dividend payments from your insurance company will be. You can then reinvest those dividends to purchase more Paid-Up Additions.

By adding a PUAR to your whole life insurance policy, you front load it to maximize its potential over the course of your lifetime.

Disclaimer: The Infinite Banking Concept® is a registered trademark of Infinite Banking Concepts, LLC. We are independent of and are not affiliated with, sponsored by, or endorsed by Infinite Banking Concepts, LLC.

Why Whole Life Insurance?

Permanent life insurance, whole life included, features a unique asset that term life insurance doesn’t offer. When you buy permanent life insurance, a portion of your annual premium is reflected in a built-in savings account called cash value. You can withdraw your cash value during your lifetime, or you can borrow it from your insurance company tax-free.

In addition to your premium payment, your cash value also earns a rate of return. Depending on the type of permanent insurance you buy, this rate of return may be calculated based on sub-accounts or market indexes (like with universal life insurance), or it can be a guaranteed rate set by your insurance company (like with whole life insurance). The reason whole life insurance is preferred for an infinite banking system is that a guaranteed rate of return helps protect your cash flow from market volatility and promises steady growth.

Second, Wealth Maximization Accounts are designed with paid-up additions (PUA) riders that create instant liquidity. A paid-up additions rider allows the policyholder to “overfund” their policy in its early years to maximize growth and supercharge the policy’s earnings over the life of the account. The design of the policy, specifically how much PUA can be added, adheres to the Internal Revenue Code Section 7702, which defines maximum contribution level of a life insurance policy without the growth being taxed. (A Wealth Maximization Account is also known as a 7702 Account or a 770 Account.)

Since 1983, all life insurance policies have had a requirement called the 7-pay test. The 7-pay test measures the amount of money paid into a policy over the course of seven years, relative to the amount of insurance coverage or death benefit. If a policy passes the 7-pay test, the cash value grows tax-deferred and can be accessed tax-free. If it doesn’t pass the 7-pay text, it is classified as a modified endowment contract (MEC).

Wealth Maximization Accounts tow the line just below MEC classification, far outperforming traditional whole life insurance in terms of growth while still receiving the same tax advantages.

Infinite banking is becoming increasingly popular among American families as people look for ways to diversify wealth away from the stock market and reduce exposure to market volatility. Cash value whole life insurance is a proven strategy for growing and protecting wealth, and one that has been used by banks and corporations for decades.

While any cash value life insurance policy could be used for infinite banking, there is one type of policy structure that reigns supreme when it comes to optimizing growth with a guaranteed rate of return and potential dividends. So if you’re interested in how to start infinite banking to help accomplish your financial goals, here’s what you need to know before you schedule a consultation with an insurance agent.

Types Of Cash Value Life Insurance

When you purchase a cash value insurance policy, it provides guaranteed coverage for life, a death benefit for your heirs, and a number of living benefits for you. Those living benefits typically include liquidity, policy loans, increased cash flow, tax advantages, and certain asset protections. When you pay your insurance premium, a portion goes toward your death benefit (the face value of the policy) and administrative fees. The remainder is reflected in the policy’s built-in savings account, called cash value.

Depending on what type of cash value life insurance you buy, you cash value grows based on one of the following:

A guaranteed rate of return (whole life)

Indexes, like the S&P 500 or Nasdaq (universal life)

Sub-accounts selected by your insurer, comparable to mutual funds (variable life)

The type of cash value policy you choose determines how much risk your “bank” is exposed to. With a universal or variable policy, growth is linked to market factors. While you might outperform the growth of a whole life policy in some years, other years could see your cash value stagnate. If you’re looking for reliable and predictable growth, a whole life policy is best suited for infinite banking.

Participating Vs. Non-Participating Whole Life Insurance

Just about any insurance agent will happily sell you a whole life policy, but not all whole life policies grow the same way. While any will provide a guaranteed rate of return, only participating whole life policies earn dividends. A participating whole life policy is one issued by a mutual insurance company. These types of insurance companies prioritize their policyholders and pay out non-guaranteed dividends in addition to a guaranteed rate of return.

The mutual insurance companies we work with at Paradigm Life have historically paid out dividends for over 100 years. What’s more, dividends are usually tax-free and can be used to pay your insurance premium or even buy additional insurance in the form of paid-up additions.

The Paid Up Additions Rider

Insurance riders are supplemental insurance that help customize your policy to deliver maximum lifetime benefits based on your financial goals and your insurance needs. When you start infinite banking, one of your priorities should be to grow the cash value in your “bank” as quickly and exponentially as possible. The paid-up additions rider allows you to do that.

In the early years of your policy, it allows you to buy additional insurance with premium payments that go directly toward cash value. Once you earn sufficient dividends with your participating whole life policy, they can be used to pay for your paid-up additions. This feature is ultimately what allows an infinite banking strategy to work so well that its growth is comparable to gains from mutual funds or qualified retirement plans after their associated taxes and fees. When your policy is structured with a paid-up additions rider, it functions more like a wealth building strategy and less like life insurance.

The paid-up additions rider allows you to supercharge your policy for rapid growth and maximum wealth over the life of the policy. It’s crucial to the success of an infinite banking strategy, so it’s imperative that you work with an insurance agent who is familiar with this type of insurance rider. They also must know how to perform the 7-pay test (adhering to Internal Revenue Code Section 7702) to safeguard your policy from becoming overfunded to the point that it becomes a modified endowment contract, or MEC, and loses its tax-advantaged status.

The Policy Loan

You can access the cash value of your whole life insurance policy at any time, for any reason, including real estate purchases, tuition, other investment opportunities, business capital, emergency expenses… you name it. But to take full advantage of the Infinite Banking concept, it’s best to use your cash value in the form of a policy loan rather than a withdrawal.

When you utilize the policy loan feature of your whole life insurance policy, your cash value continues to grow in spite of the loan. Every dollar you borrow still earns interest and potential dividends. When you pay back your policy loan, you recapture the interest—not a bank. This is the backbone of the Infinite Banking concept; your wealth continues to grow, even as you borrow against it. You are basically borrowing from yourself.

Additionally, policy loans are tax-free. You can use the interest and dividends you’ve earned without paying taxes on that money. Comparatively, if you withdraw your cash value, any amount over your basis—the amount you’ve contributed in insurance premiums—will be taxed.

In terms of paying back your policy loans, you function as your own banker and get to decide the payment schedule. Any unpaid loans will be deducted from your death benefit.

Infinite Banking And The Hierarchy Of Wealth

A participating whole life insurance policy structured with a paid-up additions rider—also known as a Wealth Maximization Account™—is the best tool for infinite banking. But it’s just the foundation of your wealth strategy, not where all your wealth is stored.

The Hierarchy of Wealth is an outline for classifying assets in terms of risk and control, offering the highest benefit for each class (rate of return). The more control you have over an asset, the less risk you have. When you start infinite banking with a Wealth Maximization Account (WMA), you’re getting optimal control, protection, and a great return. Aim to put 15-20% of earned income, or 6-24 months of living expenses into the cash value of your WMA to secure your foundation, or Tier 1 assets.

Once you’ve established your Wealth Maximization Account, you can move on to higher tiers on the Hierarchy of Wealth. Tier 2 seeks out investments that offer control, collateral, cash flow, and consistency. These investments could include your own personal development to make more money, investing in your business, or hard assets like residential real estate.

Tier 3 investments offer no guarantees and no control, or are investments where control is relinquished to a professional like a financial planner or broker. They provide higher returns, but come with higher risk. Examples include hard money lending against collateral, or syndicated funds for hard assets such as real estate or commodities.

Tier 4 investments also offer no guarantees. These are speculative investments where you risk losing 100% of your investment. This tier comes after at least 90% of your assets are in their respective Tiers 1, 2, and 3.

When you employ the Hierarchy of Wealth with a Wealth Maximization Account as your foundation, it will make you wealthy. It’s the opposite of the approach most people take with their wealth, where the riskiest assets have become their financial foundation. When a recession or market downturn comes, most people risk becoming financially wiped out, while those with an infinite banking strategy are able to take advantage of opportunities and do very well.

How To Fund Your Infinite Banking System

Although participating whole life insurance is the preferred vehicle of a successful infinite banking system, it’s important to understand your primary goal isn’t the policy’s death benefit. Yes, you’re buying insurance, but the idea is to purchase the smallest death benefit possible while contributing the maximum-allowed amount by the IRS and retain tax advantages. You’re using insurance as your bank first and as an insurance policy second.

Whole life insurance is substantially more expensive than term life insurance of the same face value, but with whole life insurance, only a portion of your premium is going toward paying for the death benefit. The rest is in your “bank” as cash value, earning interest and dividends. Plus, where term insurance is a “use it or lose it” financial tool, participating whole life insurance provides lifetime guarantees.

A Wealth Maximization Account functions as your financial foundation. Instead of cash sitting in a bank, it will be in an account that earns a greater rate of return. Unlike a qualified retirement plan, it retains liquidity and you won’t be penalized for accessing your cash value, regardless of your age or how much wealth you’ve accumulated. If you need to borrow against your insurance policy to take advantage of a purchase or investment opportunity, it comes with a guaranteed loan provision, of which you determine the pay-back schedule. And when you pass away, there is a death benefit payout.

A Wealth Maximization Account by itself won’t make you wealthy. But when you factor in the benefits, including tax benefits, low costs, liquidity, rate of return, protection from market volatility, protection from creditors and no limit to yearly contribution amounts (like with a 401k), it’s easy to see why executives, banks, corporations, and wealthy individuals rely on the infinite banking system to help grow and protect their wealth.

Infinite Banking With Paradigm Life

The expert Wealth Strategists at Paradigm Life not only understand how infinite banking with a Wealth Maximization Account works, they own WMAs themselves and have first-hand experience using whole life insurance as a financial foundation. They’ve worked with thousands of clients to set up participating whole life policies properly structured to help them reach their financial goals.

Now it’s your turn.

Request a free consultation with a Paradigm Life Wealth Strategist today to find the right whole life insurance policy to help you achieve your financial goals.